This is my first public post on a stock purchase of mine and why I like it. This post is likely wrong, probably has incorrect facts and dodgy analysis. This is produced from my scratchy notes and quick numbers. This post is not financial advice. Do your own research. 🚀🌚

The Business

Pureprofile is a business that conducts online market research, capturing data and insights via its global panel, operates a self-service SaaS portal for insight capturing and also uses its data to provide insights to media and ad agencies.

The business went through a capital raise at 2c per share (based on a discount to the share price at time of 2.4c). This capital raise was in November and December 2020, and the share price is still holding as of today (2.6c at time of writing on 25/2/21).

The Chairmans Address to Shareholders on 29th January 2021 notes that EBIT is to be at upper end of guidance of $2.5-3m, so can say that it should be close to $3m EBIT for the year (with current market cap of ~$27.5m!).

Why PPL

This stock is of interest due to me for a few points:

- The debt the business was saddled with (was $20m at 20% interest!) is now generally cleared (now $3m at 8.5%).

- Used Covid-19 to dramatically restructure their cost base (down 25%).

- The business market cap is at essentially 1x revenue.

- The SaaS platform (the “Platform”) that they have been growing.

- FY20 Q1: $110k

- FY20 Q2: $114k (4% Growth QoQ)

- FY20 Q3: $131k (9% Growth QoQ)

- FY20 Q4: $142k (8% Growth QoQ)

- FY21 Q1: $233k (64% Growth QoQ)

- FY21 Q2: $200k (14% Decline QoQ)

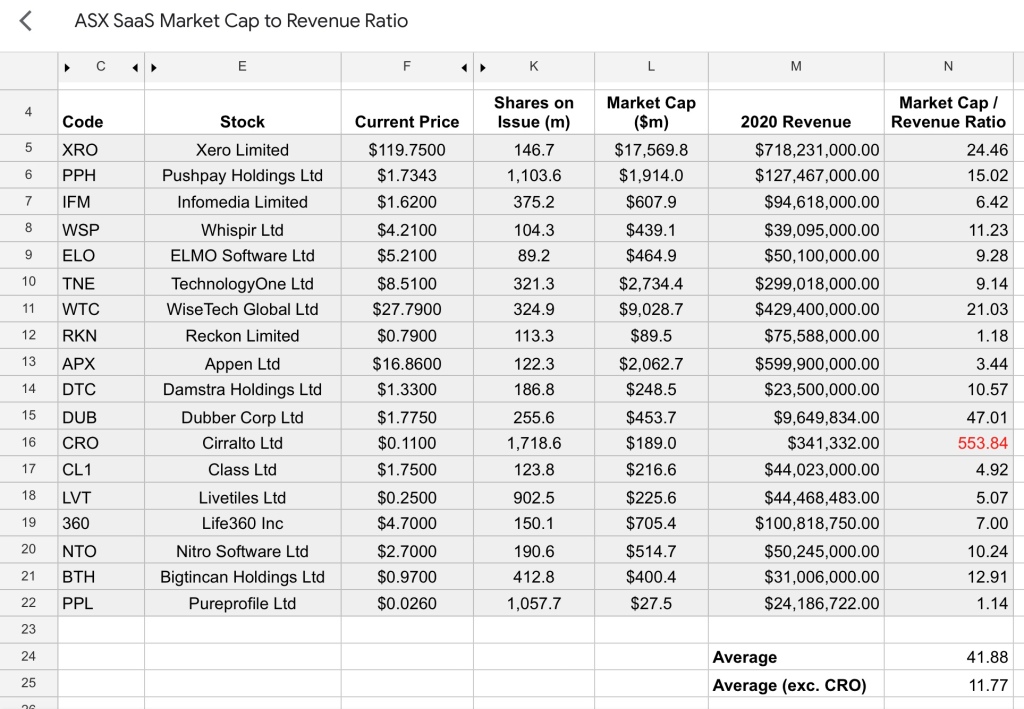

Based on a sample of an assortment of ASX SaaS businesses revenue multiples compared to market cap, the multi on average comes out to 11.77 (excluding CRO’s ridiculous multiple).

Analysis of ASX SaaS Market Cap to Revenue Ratios (as of 25/2/21)

If PPL can achieve another 75% growth for the year of the SaaS Platform business, we’d be looking at a market cap just for the Platform component of the business of ~$20m. If a 118% growth, ~$25m market cap - what the entire business is nearly valued at now.

This is excluding the other profitable, and potentially growing revenue streams - based on international expansion and general sales growth after a tough year in 2020.

Valuation

If we just value the Platform component at the the current ~$1m annualised rate, and then add the remainder of the business at 1x revenue, we’d be at a market cap of:

Market Cap = ( ARR for platform x 11.77 ) + ( ( ( Q1 Revenue + Q2 Revenue ) x 2 ) - ( ( Q1 Platform Revenue + Q2 Platform Revenue ) x 2 ) )

= ( ( $433k x 2 ) x 11.77 ) + ( ( ( $6.4m + $8.2m ) 2 ) - ( ( $233k + $200k ) 2 ) )

= $38.5m

With 1,057,734,594 shares on issue, this is a share price of 3.6c per share.

And that is valuing the non-Platform business at 1x and the Platform at 11.77x on current revenue.

If we can see growth of the non-Platform business of 30% (looks doable based on Q2 update) and 75% for Platform, the market cap would look like:

Market Cap = ( ARR for platform x 11.77 x Growth ) + ( ( ( Q1 Revenue + Q2 Revenue ) x 2 x Growth ) - ( ( Q1 Platform Revenue + Q2 Platform Revenue ) x 2 x Growth ) )

= ( ( $433k x 2 ) x 11.77 x 1.75 ) + ( ( ( $6.4m + $8.2m ) 2 1.3 ) - ( ( $233k + $200k ) 2 1.75 ) )

= $54.3m

Or a share price of 5.1c per share.

And if we can actually get the non-Platform business valued at something more than 1x (say 2x):

Market Cap = ( ARR for platform x 11.77 x Growth ) + ( ( ( Q1 Revenue + Q2 Revenue ) x 2 x Growth x Multiplier) - ( ( Q1 Platform Revenue + Q2 Platform Revenue ) x 2 x Growth ) )

= ( ( $433k x 2 ) x 11.77 x 1.75 ) + ( ( ( $6.4m + $8.2m ) 2 1.3 2 ) - ( ( $233k + $200k ) 2 * 1.75 ) )

= $92.2m

Or a share price of 8.7c per share.

Summary

- My target share price for the near term is 3.6c - based on properly valuing the Platform (SaaS) component of the business.

- For the medium term, a 5.1c per share is achievable based on current growth.

- If the non-Platform component of the business is valued at something more than 1x revenue, even just a 2x, we’d be looking at a share price of 8.7c.

Comments (1)

After my analysis, it got to a peak of 8c in Nov 2021. Currently (27 Mar 2025) it is 3.7c.

Leave a comment